Understanding Tax Obligations When Freelancing for Crypto

Freelancers earning in cryptocurrency must navigate a complex intersection of tax law and digital assets. In many jurisdictions, including the United States, the IRS classifies cryptocurrency as property, not currency. This means that receiving crypto as payment is treated as income and must be reported on your tax return. For example, if you complete a $1,000 freelance project and receive 0.02 BTC in payment, you are required to report $1,000 as income, regardless of whether you convert the Bitcoin to fiat. The USD value is determined at the time of receipt, using a reliable exchange rate source like Coinbase or CoinMarketCap.

Tracking Income and Fair Market Value

Accurate recordkeeping is the backbone of compliance. Freelancers should log every crypto transaction, including the date received, amount, and fair market value in local currency. For instance, if you completed work on June 12 and were paid 0.015 ETH, you must find its exact USD value on that day—say $2,600 per ETH, making your income $39. This transaction and its value should be recorded and backed with documentation such as invoices, contract agreements, and wallet screenshots. Using crypto portfolio management tools like CoinTracker or Koinly can automate much of this data collection and ensure consistency across reporting periods.

Capital Gains and Holding Periods

In addition to income tax, freelancers may face capital gains taxes when selling or converting received crypto. The gain or loss is calculated as the difference between the fair market value at the time of receipt and the value at the time of sale. For example, if you receive 0.01 BTC worth $300 for freelance work and later sell it for $400, you’ve made a $100 short-term capital gain (taxed as ordinary income if held under 1 year). However, if you held it for over a year, it may qualify for long-term capital gains rates, which are typically lower. This distinction is critical when planning your crypto disposition strategies.

Choosing the Right Legal and Tax Structure

Setting up a formal legal structure can greatly simplify compliance. Many crypto freelancers operate as sole proprietors, but others may benefit from forming an LLC or S-corp, especially if their earnings exceed $50,000 annually. These entities can unlock tax deductions, limit liability, and facilitate better recordkeeping. For example, a US-based freelance developer earning $80,000 in crypto annually might form an S-corp to reduce self-employment taxes by paying themselves a reasonable salary and taking dividends. Always consult with a licensed tax advisor or accountant who understands crypto-related business structures.

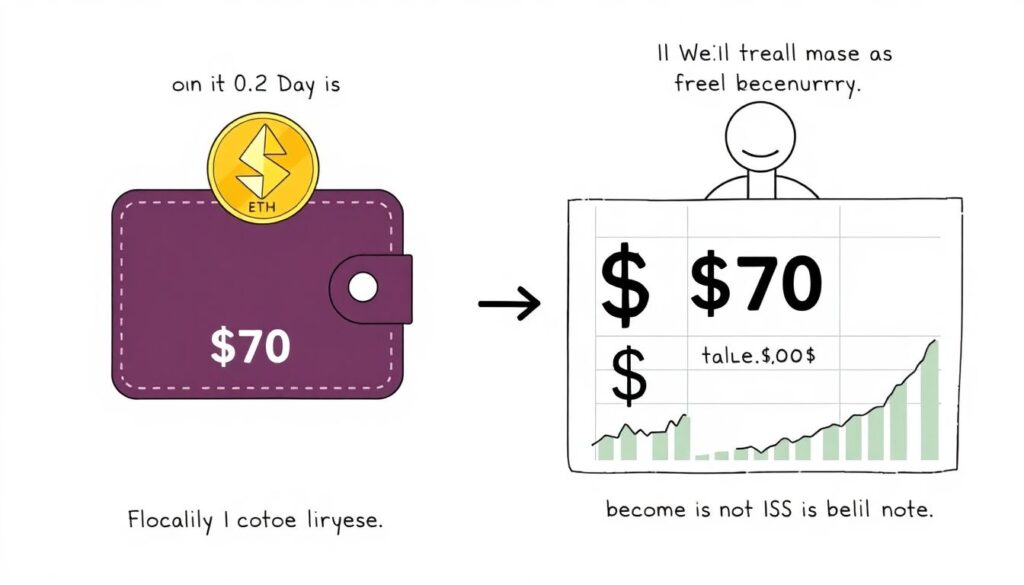

Dealing With Volatility and Tax Implications

One unique challenge of earning in crypto is volatility. A freelancer might receive 0.02 ETH worth $70 one day, only to see it drop to $50 before converting it to fiat. Unfortunately, the IRS still considers the $70 value as taxable income at the time it was received. This disconnect between income valuation and real-world conversion can lead to tax liabilities that exceed actual fiat proceeds. To mitigate this, some freelancers opt for automatic conversion tools available on platforms like Bitwage or accept stablecoins such as USDC, which maintain a 1:1 peg with the US dollar, reducing risk exposure and simplifying accounting.

International Perspectives on Crypto Freelance Income

Globally, tax treatment of crypto varies significantly. In the UK, HMRC treats crypto as a taxable income when received for services but also expects capital gains reports upon disposal. Germany offers tax exemption for crypto sold after a 12-month holding period, providing strategic flexibility. In contrast, India imposes a 30% flat tax on gains from crypto, without deductions. Freelancers working with international clients must be particularly cautious about double taxation. Leveraging tax treaties and understanding local crypto-specific rules is essential to avoid penalties. Tools like TaxBit and Coinpanda offer region-specific compliance support.

Invoicing, Contracts, and Proof of Work

To ensure legal and tax compliance, always use formal invoices with time-stamped records and specify “payment in cryptocurrency” in contracts. Include wallet addresses, exchange rates at the time of payment, and project milestones. For example, if you’re paid in ETH for a UI/UX design project, your invoice should state the ETH amount, its USD equivalent on the invoice date, and a link to the transaction on the blockchain (like Etherscan). Storing these documents in secure cloud storage like Google Drive or Notion helps in case of future audits or client disputes.

Anti-Money Laundering (AML) and Know Your Customer (KYC) Considerations

While many freelancers overlook it, onboarding clients without verifying their background can expose you to AML risks, particularly if you’re receiving anonymous payments. Regulatory bodies like FinCEN in the US require businesses with repeated crypto transactions to comply with AML/KYC laws. While freelancers themselves may not fall under “money service businesses,” high-volume or recurring crypto payments could draw regulatory scrutiny. Using platforms like Upwork or Deel, which handle KYC for both parties and issue tax documentation, can mitigate exposure and simplify compliance.

End-of-Year Reporting and Required Tax Forms

At the end of the fiscal year, freelancers must file income statements reflecting crypto earnings. In the US, this typically involves reporting self-employment income on Schedule C and potential capital gains on Form 8949 and Schedule D. If you earned over $400, you’ll also owe self-employment tax. Crypto exchanges may issue Form 1099-NEC or 1099-B, but often, they don’t track freelance payments accurately. Therefore, it’s your responsibility to consolidate your records. Failing to report crypto income can lead to penalties of 20–40% of unpaid tax, and repeated offenses may trigger IRS audits.

Conclusion: Staying Ahead Through Proactive Management

Remaining compliant as a crypto-earning freelancer requires more than just tracking income—it demands a proactive, structured approach to accounting, legal structure, and strategic planning. While the landscape continues to evolve, regulators are making it clear: ignorance is not an excuse. By using the right tools, engaging specialized tax professionals, and maintaining transparent records, freelancers can confidently grow their crypto-based businesses without running afoul of tax authorities.