Stablecoins sound simple on the surface: “crypto that doesn’t move.” But once you dig in, you realize they sit right at the crossroads of banking, regulation, and code. That’s why understanding how they work — and where they can break — is non‑optional if you’re just starting out.

Below is a beginner‑friendly, but technically accurate, walkthrough of what stablecoins are, why they matter, and how to use them without sleepwalking into unnecessary risk.

—

What exactly is a stablecoin?

At its core, a stablecoin is a digital token designed to track the price of something else — usually 1 USD, sometimes EUR, gold, or even a basket of assets. The goal is price stability: 1 token ≈ 1 unit of reference.

Most stablecoins fall into three big buckets:

1. Fiat‑backed (custodial)

Tokens like USDT (Tether) and USDC (Circle) are issued by a company that holds reserves (cash, short‑term U.S. Treasuries, bank deposits). In theory, every token should be redeemable for 1 USD.

2. Crypto‑backed (over‑collateralized)

Protocols like DAI lock volatile crypto (e.g., ETH) as collateral in smart contracts. To mint 100 DAI, you might need $150+ worth of ETH, forming a buffer against market swings.

3. Algorithmic or hybrid models

These rely on economic incentives, arbitrage, and sometimes partially collateralized designs to hold the peg. Some work in niche contexts; some have collapsed dramatically.

So when someone says they want to buy stablecoins, they might be talking about very different risk profiles hiding behind the same “1 USD” label.

—

Why stablecoins exploded — with some numbers

By late 2024, the total stablecoin market capitalization hovers around the $150–170 billion range, depending on the month. Tether alone represents more than half of that, with USDC taking a big chunk and the rest split among DAI, FDUSD, TUSD, PYUSD, and others.

Daily on‑chain stablecoin transfer volumes frequently exceed $50–100 billion, making stablecoins one of the most used real‑world applications of crypto, even more than many DeFi tokens or NFTs. In some emerging markets, stablecoins function as de‑facto dollar accounts for users who can’t easily access USD banking.

This isn’t just speculation volume. Remittances, merchant payments, and on‑chain trading all feed into these numbers. That’s why top stablecoin exchanges for USD deposits aggressively market to retail and institutional users: stablecoins are now a major gateway into the digital asset economy.

—

Peg mechanics: why “1 USD” is not guaranteed

Short paragraph: a peg is a *target*, not a promise.

Longer explanation: a stablecoin holds its peg through one or more of these mechanisms:

– Redemption arbitrage: If a token trades at $0.99 and you can redeem it with the issuer for $1, traders buy on the market and redeem, pushing the price up.

– Collateral buffers: Over‑collateralization ensures volatility in backing assets doesn’t immediately break solvency.

– Liquidity incentives: Protocols pay yield or fees to encourage traders and market makers to support liquidity around $1.

– Expectations and trust: If users believe others will keep treating it as $1, they’re willing to accept it as such. Once trust cracks, even well‑designed systems wobble.

When these forces fail or weaken, you see “depegs”: the price drifts to $0.97, $0.93, or worse. TerraUSD (UST) collapsing close to zero in 2022 is the textbook example of algorithmic failure combined with overconfidence.

—

Core risks beginners usually underestimate

Short list first, then details.

1. Issuer and reserve risk (custodial)

2. Collateral and liquidation risk (DeFi)

3. Smart‑contract bugs and exploits

4. Regulatory and censorship risk

5. Liquidity and market structure risk

Now the nuance.

Fiat‑backed coins depend on reserve quality. If an issuer keeps reserves in risky commercial paper, uninsured bank deposits, or opaque vehicles, a banking‑style run can occur. Transparency reports and attestation frequency matter a lot more than marketing slogans.

Crypto‑backed models like DAI or LUSD rely on collateral volatility. If ETH crashes 40% in a day and the protocol isn’t liquidated efficiently, you can end up under‑collateralized. Liquidation penalties, oracle reliability, and auction design are not trivia; they’re the backbone of peg safety.

Smart contracts introduce another layer: one bug in a DeFi protocol that holds your stablecoins can drain everything, even if the coin itself is sound. Audits reduce but don’t erase this risk.

On the regulatory side, a single jurisdiction can heavily influence a global product, because USD‑linked stablecoins touch the U.S. banking system. Issuers can be pressured to freeze, blacklist, or seize funds tied to sanctions, investigations, or compliance actions. That’s why censorship‑resistance varies dramatically between designs.

Finally, liquidity risk is often invisible until something breaks. Getting in is easy; getting out during market stress can be painful if order books are thin or withdrawal queues form.

—

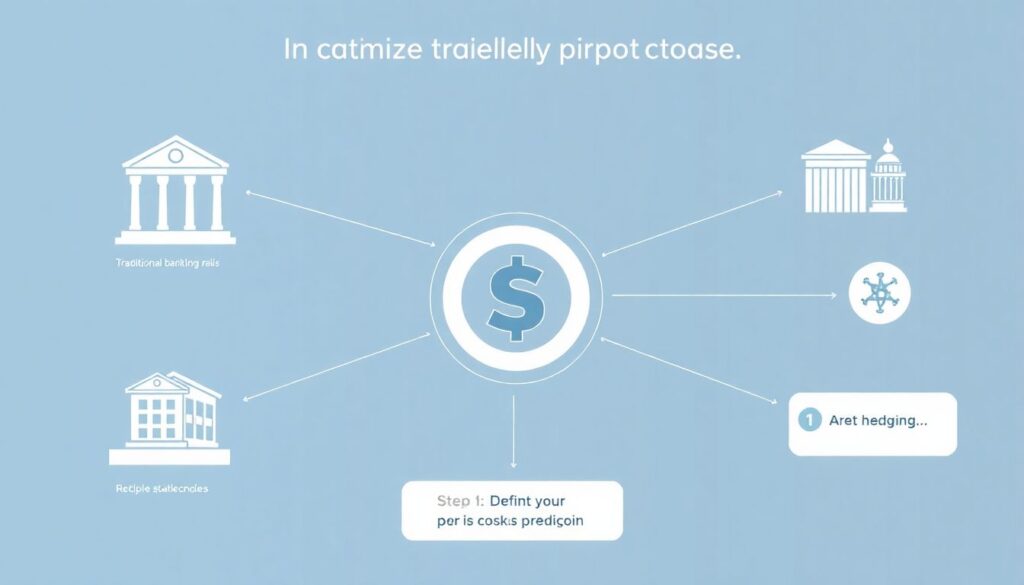

How to approach stablecoins as a beginner (with an engineer’s mindset)

Think of stablecoins like infrastructure, not just a “crypto hack.” If you’re trying to buy stablecoins with low fees, you’re essentially choosing between different combinations of banking rails, blockchains, and counterparties.

A systematic approach:

1. Define your use case precisely

Are you hedging against local currency inflation, moving money cross‑border, parking funds for DeFi yield, or just trading on centralized exchanges? Each goal points you toward different assets and platforms.

2. Segment your risk buckets

Don’t put everything into a single stablecoin. Split, for example, between a regulated fiat‑backed coin (USDC), a more aggressive but liquid option (USDT), and a decentralized alternative (DAI or LUSD). This way, a failure in one design doesn’t wipe you out.

3. Match chain choice to actual needs

Sending $50 on Ethereum mainnet is overkill when a cheap L2 or sidechain does the job. Transaction costs and finality times vary widely, and that affects your real‑world experience more than you expect.

This mindset is less “which coin is best” and more “how do I architect a small personal treasury that can survive shocks.”

—

Where to start: platforms, exchanges, and custody

Beginners tend to search for the best stablecoin platforms for beginners, but the better question is: which setups minimize *operational* and *counterparty* error.

A practical architecture might look like:

– A reputable centralized exchange for on‑ramping from bank transfers or cards.

– A non‑custodial wallet on a cheap chain (e.g., an L2) for actual usage.

– One DeFi platform you truly understand, rather than five you vaguely recognize.

When you compare top stablecoin exchanges for USD deposits, look beyond the headline fee. Evaluate:

– Jurisdiction and licensing

– History of downtime and withdrawal halts

– Clarity of user terms around stablecoin redemptions and freezes

– Whether they support direct chain withdrawals in the stablecoin you want, or force expensive conversions

Unconventional but effective tactic: test your entire flow with very small amounts — deposit → buy → withdraw → swap → send — before committing serious capital. Treat it like a fire‑drill for your own process.

—

How to invest in stablecoins safely: a layered approach

Investing in stablecoins is really about parking purchasing power, sometimes with yield. To tackle how to invest in stablecoins safely, you can build a layered model instead of going “all in” on a single yield farm.

1. Base layer: zero‑or‑low yield, maximum safety

– Reputable fiat‑backed stablecoins held in self‑custody or on a top‑tier exchange with strict risk controls.

– Objective: capital preservation and liquidity.

2. Middle layer: moderate yield, moderate complexity

– Lending stablecoins on large, audited protocols with deep liquidity (e.g., Aave, Compound on major chains).

– Objective: small incremental yield while still being able to exit quickly.

3. Outer layer: experimental yield

– Liquidity provision, structured products, or complex DeFi strategies.

– Objective: higher returns on a small slice you can afford to stress‑test.

This structure ensures a bug or a depeg in one corner doesn’t ruin your entire portfolio. It’s a risk‑engineering view rather than a pure return‑chasing mindset.

—

Chasing yield without courting disaster

Yields on stablecoin interest accounts with highest APY can be seductive, but consistently high rates usually imply:

– Leveraged borrowers on the other side.

– Token incentives that will eventually dry up.

– Hidden rehypothecation (your coins are lent again and again).

Non‑standard, conservative trick: cap your target APY. For example, decide in advance that anything above, say, 8–10% APY in a relatively calm market is automatically classified as “high risk,” no matter how it’s marketed. This simple rule filters out the most dangerous offers and forces you to ask, “Where is this extra risk coming from?”

On centralized platforms, be wary of “earn” or “savings” products where your legal claim is unsecured. If that platform fails, you are often a general creditor, not a depositor. Read the terms; if they say the company can lend, invest, or pledge your assets, treat it as a credit exposure.

—

Economic implications: how stablecoins affect money and markets

From a macro angle, stablecoins are effectively shadow dollars (or euros) sitting outside traditional deposit insurance schemes. When users move money from a bank account into stablecoins, they:

– Reduce traditional bank deposits (affecting banks’ funding).

– Increase demand for short‑term Treasuries and money‑market‑like assets held by issuers.

– Potentially speed up capital flight from weaker banking systems.

For the U.S., paradoxically, this can strengthen the dollar’s global role: people in high‑inflation countries can hold USD exposure via tokens even without U.S. bank accounts. At the same time, regulators worry about runs: if confidence in a big issuer breaks, unwinding tens of billions of assets rapidly could move short‑term funding markets.

In crypto markets, stablecoins are the base collateral for perpetual futures, options, and many DeFi protocols. Their stability directly affects leveraged positions, liquidity depth, and overall market health. A major depeg often cascades into forced liquidations and volatility spikes.

—

Industry impact and forecasts: where this is headed

Short‑term (1–3 years), it’s reasonable to expect:

– Continued growth of total stablecoin supply, potentially pushing past $250–300 billion if rates remain relatively attractive and on‑chain finance keeps expanding.

– Greater fragmentation: jurisdiction‑specific stablecoins (e.g., regulated EU‑only products), plus more non‑USD pegs.

– Tighter compliance: mandatory KYC at issuance and redemption points, more blacklisting tools, and clearer classification of stablecoin issuers (bank vs. non‑bank).

Longer term (5–10 years), stablecoins will likely coexist — and compete — with central bank digital currencies (CBDCs). The interesting possibility is that private stablecoins remain more flexible and composable for DeFi and cross‑chain use, while CBDCs stay more restricted and tightly permissioned.

For the broader industry, stablecoins are becoming:

– Settlement rails for exchanges and fintechs.

– Building blocks for tokenized assets (T‑bills, funds, invoices).

– Liquidity layers across multiple chains, acting as the “reserve asset” of on‑chain finance.

Regulatory clarity will probably shrink the number of issuers but solidify the survivors as critical financial infrastructure.

—

Non‑standard strategies for beginners who want to be careful, not paranoid

To wrap up, a few unconventional but practical tactics you can apply right away:

1. Simulate a failure scenario on paper

Pick your main stablecoin. Imagine it suddenly trades at $0.80 and withdrawals from your favorite platform are halted. Write down, step by step, what you would do, with which backups, and how fast. If the plan looks messy, simplify your setup.

2. Use time‑based diversification, not just asset diversification

Instead of converting a large amount into stablecoins on a single day, spread it over weeks. This reduces timing risk around regulatory news, market stress, or technical incidents.

3. Treat platforms as vendors, not as “homes”

Don’t emotionally commit to a particular app or exchange. If fees rise, transparency drops, or risk increases, be ready to migrate calmly. Maintaining that detachment prevents you from rationalizing obvious red flags.

4. Build a “sleep test” threshold

If a particular strategy or yield would make you anxious watching prices for days, scale it down until you’d be comfortable ignoring it for a month. This is a surprisingly effective sanity check on your risk level.

If you combine these habits with basic due diligence on issuers, protocols, and platforms, you’ll be far ahead of most new users. Stablecoins aren’t inherently safe or dangerous; they’re tools. The edge comes from understanding *what* you hold, *how* it’s backed, and *who* has power over it — and then structuring your usage accordingly.