Why stablecoin reserves and operations actually matter

If you hold or trade any crypto, you’re already relying on stablecoins, даже если это не сразу заметно. They sit in the middle of exchanges, DeFi protocols, and OTC deals as the “digital cash” layer. The catch is simple: a stablecoin is only as good as its reserves and the people running it. If the backing is weak or the operations are sloppy, your supposedly “stable” token can de-peg in hours. A beginner-friendly stablecoin due diligence guide starts with one core idea: you’re not just buying a token, you’re trusting a balance sheet and an operating company. Treat it like evaluating a small private bank that issues its own digital dollars, not like buying a meme coin.

Key definitions before you dive into the numbers

What is a stablecoin, really?

At a high level, a stablecoin is a token designed to track the value of some relatively stable asset, usually USD or EUR. On paper that sounds trivial, but the way the peg is achieved can be radically different. Fiat-backed coins keep money and short-term assets off-chain in bank accounts and custodians. Crypto‑collateralized stablecoins rely on overcollateralized on-chain positions. Algorithmic models attempt to hold the peg using incentives and supply adjustments instead of hard collateral. When someone asks how to evaluate stablecoin reserves, they’re really asking how to judge whether that peg mechanism can survive stress, panic and black-swan events, not just quiet market days.

What do “reserves” actually mean?

Reserves are the assets that are supposed to cover all outstanding stablecoins, ideally at a 1:1 ratio or better. For a fiat-backed USD token, that might be cash in bank accounts, overnight repo, T‑Bills or money market funds. For a crypto-backed design, reserves are on-chain collateral locked in smart contracts. The core question is simple: if everyone redeemed at once, would there be enough high‑quality assets to pay them back without delay? When you start reading stablecoin transparency and reserve reports, look for clear breakdowns of assets, maturities and counterparties, not just a total headline number that says “we’re fully backed, trust us”.

Basic mental models: how different stablecoins keep their peg

Fiat-backed vs crypto-backed vs algorithmic

An easy way to visualize this is a triangle of design choices. One corner is fiat-backed: think USDC‑style, where each token should be backed by “real world” financial assets. Another corner is crypto-backed, like DAI, which holds volatile assets such as ETH but uses overcollateralization to stay safe. The third corner is algorithmic: the system tries to maintain $1 by expanding or contracting supply using incentives, without fully matching each token with collateral. [Diagram in text: imagine a triangle labeled “Fiat reserves,” “On-chain collateral,” and “Algorithms.” Each stablecoin sits somewhere inside this triangle depending on its design.] As you move away from hard collateral toward algorithms, potential yield might rise, but so does systemic risk.

Different risk profiles at a glance

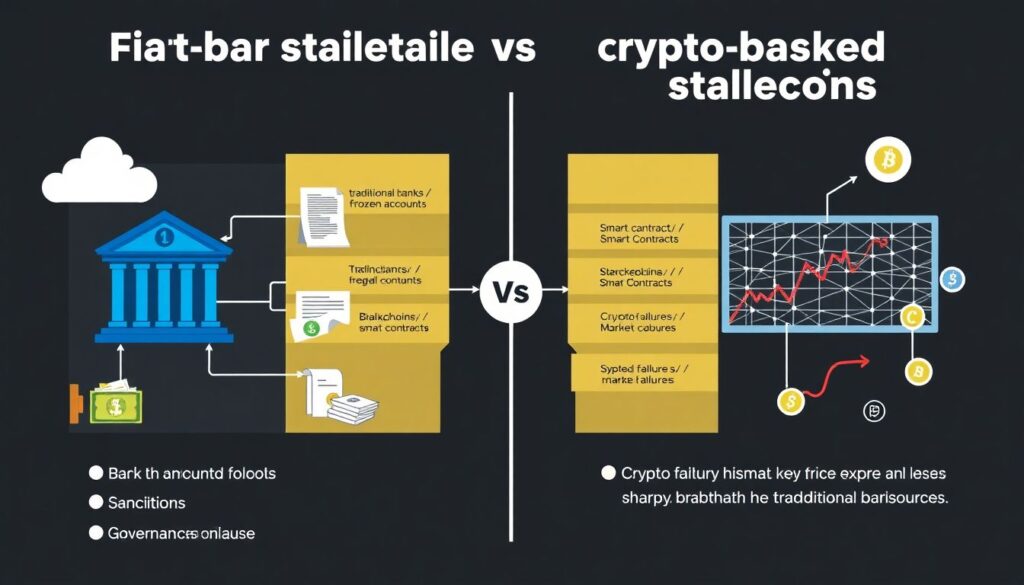

Fiat-backed stablecoins rely heavily on banking rails and regulators. Their main threats are bank failures, frozen accounts, sanctions and governance abuse. Crypto-backed ones are more exposed to smart-contract bugs, oracle failures and market crashes, but less to bank runs in traditional finance. Algorithmic models, as history kindly demonstrated, are vulnerable to confidence shocks: if users no longer believe in the mechanism, the peg can unravel extremely fast. Any serious stablecoin risk assessment for investors has to ask not only “what backs this?” but “what can go wrong in this particular design, and who has the power to push the big red buttons when things break?”

How to read and compare reserve quality

Asset composition: cash, bonds, and everything in between

When people talk about the best stablecoins with audited reserves, they’re usually praising a specific mix of assets: mostly cash and very short-term government securities, with minimal exposure to corporate debt, commercial paper or exotic instruments. [Diagram in text: picture a horizontal bar split into segments: “Cash,” “T‑Bills < 3 months,” “Other highly liquid,” “Risky / illiquid.” The farther to the right the bar extends, the riskier the reserve.] If the breakdown shows a large share of long-dated bonds, loans, or anything described with vague words like “other investments,” assume higher risk. High yield on reserves almost always means someone, somewhere in the structure, is taking extra risk; that might ultimately be you.

Location and custody of reserves

Reserve quality is not only “what” but also “where” and “who holds it”. Funds spread across multiple reputable banks and regulated custodians are less fragile than money piled into one offshore institution. Compare two scenarios: in the first, reserves sit in a single small bank in a loose-jurisdiction; in the second, they are diversified across major US or EU banks plus treasury custodians. The second option may be more boring, but it’s usually safer. [Diagram in text: imagine two circles; one small circle labeled “Single Bank” and one made of several smaller circles connected, labeled “Diversified Custody.” The multi-circle setup indicates lower single-point-of-failure risk.]

Operational model: who can press which buttons

Centralized issuers vs protocol-based systems

Centralized issuers have a company behind the stablecoin. They can freeze addresses, blacklist funds, or halt redemptions if regulators knock on the door or internal risk triggers fire. On one hand, that can protect the system against hacks and obvious abuse. On the other, such control introduces censorship and governance risk, especially if the company is lightly regulated or opaque. Protocol-based stablecoins encode most rules in smart contracts, so redemptions and liquidations follow transparent logic. However, there are still upgrade keys, governance tokens, multisigs and emergency powers. [Diagram in text: a slider from “Full corporate control” to “Fully automated protocol,” with most real projects somewhere in the middle rather than at the extremes.]

Redemption mechanics and liquidity in practice

Even if reserves are strong, you care about how fast you can exit. Can regular users redeem directly for fiat, or is that privilege limited to big institutions with KYC and large minimums? If you can’t redeem but whales can, you’re exposed to secondary market swings while they quietly exit at par. Also, watch on-chain liquidity: large stablecoin/USDC or stablecoin/ETH pools tell you how much slippage you’ll face if you dump in a panic. A robust design shows deep liquidity on major exchanges and DeFi venues, plus a clear, tested redemption path that has handled stress, not just sunny-day flows during bull markets.

Step-by-step: how to evaluate stablecoin reserves as a beginner

Start with public documentation and audits

For a beginner, the first checkpoint is basic disclosure. Does the issuer publish monthly or even weekly reports? Are they signed by a known audit or attestation firm, or just by the company itself? Try to see at least a year of history to understand whether disclosures are consistent, detailed and timely. A practical how to evaluate stablecoin reserves process might look like this: grab the latest report, check the total outstanding supply on-chain, see whether assets slightly exceed liabilities, read the footnotes regarding what counts as “cash equivalents,” and look up the auditor’s reputation. When something feels vague or heavily marketed rather than factual, treat it as a yellow flag, especially if large sums are involved.

Cross-check on-chain and off-chain data

Many centralised stablecoins publish their smart contract addresses. That lets you verify how many tokens are actually in circulation. Compare that on-chain number with claims in the latest reserve report. If they’re misaligned or explanations are missing, that’s a problem. For crypto-backed models, examine collateralization ratios on dashboards: see how much collateral backs each token, how diversified it is and whether liquidations have worked before. [Diagram in text: imagine two columns, one titled “On-chain Supply,” the other “Reported Assets.” An arrow connects them; if the numbers closely match and move in sync over time, trust increases.]

Comparing three main approaches to stablecoin design

Fiat-backed: stability with regulatory and counterparty exposure

Fiat-backed coins tend to offer the most familiar risk structure for traditional finance people. The reserves sit in bank accounts and short-term instruments; the company earns yield, while token holders get convenience. The upside is usually a very tight peg, especially if redemptions are open and frequent. The downside is dependence on regulators, banking partners and corporate governance. Freeze orders, sanctions lists and blacklisting can all hit you indirectly. When two fiat-backed coins compete, the one with more granular disclosures, independent audits and better jurisdictional setup usually deserves a higher trust score, even if its brand is smaller or its market cap is more modest.

Crypto-backed: transparency with market and technical risk

Crypto-backed models like DAI appeal to users who prefer trust-minimized systems. You can inspect vaults, collateral types and liquidation rules on-chain. If the design is conservative—heavy use of stables and government-bond tokens as collateral instead of pure volatile assets—risk can be quite controlled. But you’re still exposed to bugs, oracle manipulation and liquidity crunches in the underlying collateral. These systems also tend to cap scalability: you can’t print infinite stablecoins without finding more acceptable collateral. In practice, well-designed crypto-backed coins feel safer to technically savvy users, while newcomers might find them complex and harder to understand than simple “token equals one dollar in the bank” narratives.

Algorithmic and partially collateralized: high innovation, high danger

Algorithmic and undercollateralized coins usually promise attractive yields and capital efficiency. They rely on incentives, arbitrage, and supporting tokens that are supposed to absorb volatility. History shows that when sentiment turns, these mechanisms can spiral: redemptions surge, governance tokens tank, collateral value collapses and the peg dies. The big collapses weren’t just accidents; they revealed a structural weakness: confidence is a form of collateral, and it can vanish overnight. For beginners, these coins might be interesting to study as engineering experiments, but they’re a dangerous place to park savings. Treat them more like high‑risk DeFi strategies than digital equivalents of cash.

Using transparency and reports without being fooled by them

What good reporting looks like

Solid projects don’t just dump PDFs; they build habits. You should see regular, time-stamped updates, consistent methodology, and clear reconciliation between balance sheet items and token supply. Good reports break down asset classes by maturity, credit quality, and jurisdiction, and they explain changes over time—why commercial paper went down, why T‑Bill exposure increased, and how that affects risk. They may also disclose stress tests: what happens if rates spike or a bank partner fails. If you feel you can follow the narrative from report to report like a story, that’s a good sign. If each document looks like a marketing brochure with little hard data, reserve some skepticism.

Red flags even beginners can spot

You don’t need to be a CFA to notice warning signs. If the issuer fights with regulators, delays reports, changes auditors too often, or posts vague one-page “attestations” every few quarters, that’s a pattern. If supply grows rapidly during bull markets but reporting does not keep pace, ask yourself whether reserves are actually following. A simple mental check: imagine a bank explaining its balance sheet with the same level of detail; would you keep your life savings there? If the answer is no, consider reducing exposure or diversifying into alternatives with better disclosures and a calmer, more boring operational history.

Practical checklist for beginners doing stablecoin due diligence

Balancing convenience, risk and ideology

When you assemble your own stablecoin mix, you’re really choosing a trade-off between convenience, censorship resistance, transparency and technical risk. A fiat-backed coin from a large, regulated issuer might be your default for payments and CEX trading. A crypto-backed option might be your choice for DeFi positions if you worry about blacklisting. You can also keep a small experimental bucket for new algorithmic designs, treating that as speculative capital, not your core cash. Over time, your personal “portfolio” of stables becomes a living example of applied risk management, updated as markets, regulations and technologies change around you.

Investor-focused risk lens

From an investor’s standpoint, reserve and operational due diligence is simply non‑optional. That’s why a simple phrase like stablecoin risk assessment for investors hides a complex process involving legal, technical and financial review. Retail users can copy a lighter version of that: stick to projects with long operating history, transparent and frequent audits, diversified reserves and clear redemption mechanics; avoid anything that spikes in yield without clear explanation of where that extra return comes from. And if a project matches most of your boxes but still feels “off,” it’s fine to pass. In the world of digital dollars, there are enough options that you don’t need to force yourself into designs you don’t fully understand or trust.

Wrapping up: turning information into action

From theory to your own decision-making framework

By now you’ve seen that evaluating a stablecoin is less about memorizing buzzwords and more about building a simple internal framework: what backs it, who holds it, who controls it, and how you get in and out under stress. Use public audits, chain data and issuer communication as your raw material, filter them with a bit of skepticism, and compare different designs side by side. Over time you’ll develop your own informal ranking of trustworthy coins, your personal list of the best stablecoins with audited reserves, and a sense for when new projects are worth the experimental risk. That’s how a beginner moves from blind reliance on marketing to an independent, disciplined approach to stablecoin analysis.